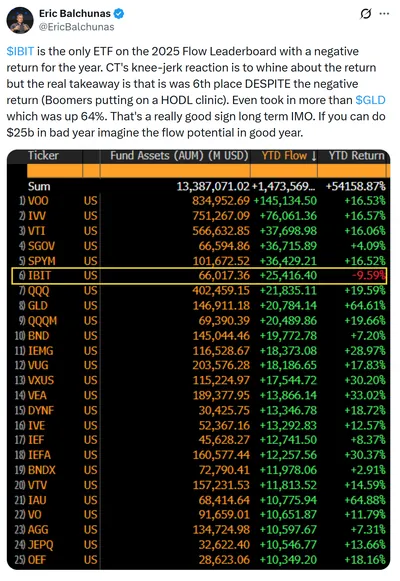

Delaware Life Insurance Company has launched a fixed indexed annuity that links potential returns to Bitcoin’s price movements, marking a new bridge between traditional insurance products and digital assets. Announced in Wilmington, Delaware, in early 2025, the product provides Bitcoin exposure not by holding coins directly but by using BlackRock’s spot Bitcoin ETF, IBIT, a fund approved by the U.S. Securities and Exchange Commission in early 2024. Bloomberg ETF analyst Eric Balchunas confirmed the strategic development, highlighting the partnership’s significance for both the insurance and crypto sectors.

Overview of Delaware Life’s Bitcoin-Linked Annuity

The new annuity is structured as a fixed indexed annuity that offers a guaranteed minimum return alongside the opportunity for additional credited interest tied to an index that reflects Bitcoin’s price performance. Delaware Life accomplishes Bitcoin exposure through allocations to shares of BlackRock’s iShares Bitcoin Trust (IBIT), rather than by taking custody of private keys or directly holding cryptocurrency. This arrangement pairs a familiar retirement vehicle with an exchange-traded proxy for Bitcoin, combining insurance features with digital-asset exposure; for more on BlackRock’s role with IBIT, see BlackRock and IBIT.

How the Bitcoin-Linked Annuity Works

Functionally, the annuity credits interest based on the performance of the chosen reference — in this case, a path to Bitcoin price moves via the IBIT ETF — while guaranteeing a minimum contract value to protect principal from downside market losses. Policyholders do not receive direct Bitcoin ownership; instead, the insurer’s use of IBIT provides an ETF-traded price reference that determines the indexed crediting. The product retains typical annuity features such as tax-advantaged treatment within retirement planning and contractual protections for the guaranteed portion of the investment.

Broader Implications for Traditional Finance

This launch exemplifies how established financial firms are incorporating spot Bitcoin ETFs into regulated products offered by insurance companies, expanding avenues for investors who prefer regulated wrappers over direct crypto custody. BlackRock’s participation and the ETF’s regulatory approval add institutional credibility to that path, which could influence how other insurers evaluate similar offerings; readers can find related discussion of IBIT’s role in traditional products via IBIT investment theme. At the same time, the annuity targets clients seeking retirement exposure to alternative assets while keeping familiar insurance protections in place.

Expert Analysis and Risk Considerations

Market commentators note that embedding an ETF like IBIT into an annuity provides a regulated, custodial route to Bitcoin-linked returns and benefits from BlackRock’s operational scale. Nevertheless, the upside portion tied to Bitcoin remains exposed to price volatility, and the product does not confer direct ownership of cryptocurrency. Potential buyers should evaluate specific product mechanics — including any caps, participation rates, and the guaranteed floor — to understand how much upside participation they will actually receive versus what is protected.

Why this matters (for a miner in Russia)

If you operate between one and a thousand mining devices in Russia, this product does not change how you run your rigs or how Bitcoin is mined. What it does offer is an additional, regulated way to get retirement exposure to Bitcoin’s price movements without managing private keys or self-custody. For miners considering long-term allocation of earnings into retirement vehicles, the annuity may be an option to convert mining proceeds into a structured, insured product that still references Bitcoin’s market performance.

What to do? (practical steps for miners)

- Compare exposures: weigh the difference between keeping mined BTC, buying spot ETF shares personally, or using a regulated annuity that references IBIT.

- Read product terms: examine caps, participation rates, guaranteed minimums, fees, and surrender conditions before committing funds.

- Consider tax and reporting: consult a local advisor about how converting mining income into annuity contributions interacts with your tax and accounting situation in Russia.

- Start small: if interested, test allocation with a modest portion of mining proceeds while you learn how the annuity credits returns tied to IBIT.

Frequently Asked Questions

How is Bitcoin exposure structured in this annuity?

The annuity links a portion of its potential interest credits to the performance of the BlackRock iShares Bitcoin Trust (IBIT). Delaware Life allocates funds to the ETF, and the policy’s credited value can increase if IBIT’s price rises, subject to the annuity’s specific terms such as caps or participation rates.

Is my principal safe with this Bitcoin-linked annuity?

As a fixed indexed annuity, the contract includes a guaranteed minimum value that protects principal from market loss tied to Bitcoin declines. However, any additional growth linked to Bitcoin performance is not guaranteed and can vary according to market moves and the product’s crediting formula.

Why use BlackRock’s IBIT instead of buying Bitcoin directly?

Using IBIT lets the insurer offer Bitcoin exposure within a regulated, custodial framework without managing private keys or relying on cryptocurrency exchanges for direct custody. That structure fits the operational model of insurance companies and the contractual nature of annuities.

Who is the target customer for this product?

The annuity targets retirement-focused investors who want exposure to Bitcoin’s potential upside but prefer it wrapped within an insurance product that provides a guaranteed floor and other annuity features.

Could other cryptocurrencies be added to annuities later?

The current product focuses on Bitcoin through IBIT. The same product architecture could in principle be adapted for other digital assets if similarly regulated spot ETFs become available and gain institutional acceptance.